The Pinnacle: February 2023

F E B R U A R Y 2 0 2 3 • I S S U E 2 7

Market Review

In February, strong economic data led to bond yields moving higher and a weaker equity market. With developed market equity down 2.4% for the month, investors were disappointed with a hawkish US Federal Reserve (Fed) outlook, which indicates that there is still some uncertainty ahead regarding the end of the rate hiking cycle. During the first week in March news broke that Silicon Valley Bank (SVB), a bank that caters predominantly to the technology industry, collapsed. This came after some turbulent days where the bank had tried to raise capital urgently, to meet the demand of customers deposit withdrawals, by selling liquid assets at a loss. During the 2020 – 2021 technology boom the bank had invested large proceeds received into long-term treasury bonds at the then lower interest rates, which has since risen and pushed the price of these bonds down due to the inverse relationship between bond yields and their price.

The major US market indices ended the February in the red. This comes as the month had been the month when the narrative largely changed concerning the Fed, the end of the rate hiking cycle and the possibility of the start of reducing rates. Towards the end of last year and January of this year, the market was pricing in expected rate cuts before the end of this year. The changing of this narrative came as Fed Chairman, Jerome Powell, warned that the process of disinflation still has a long way to go with the Fed expected to raise rates further and keep them higher for longer. While economic data, especially in the labour market continues to come in strong, this would support the higher-for-longer narrative as the Fed believes it must weaken the economy to bring down inflation to meet its 2% target.

As expected, the Bank of England (BoE) raised rates by 50 basis points at the start of February. The accompanying statement was dovish with BoE governor, Andrew Bailey, declaring that inflation has turned a corner in the UK. January’s inflation numbers came in at 10.1% year-on-year (YoY) down from 10.5% in December. A significant improvement in the Purchasing Managers Index (PMI) business surveys as well as consumer confidence added to positive sentiment in the UK in February. This led to the FTSE 100, an index consisting of 100 publicly traded companies in the UK, seeing its largest February gain since 2019, of 1.3%. Despite this, it is important to be cognisant of the fact that the longer positive economic data is seen (except inflation coming down) the more likely the BoE is to keep rates higher for longer, just as in the US.

The European Central Bank (ECB) raised rates by 50 basis points in February while confirming its intention to do the same in March. The ECB seems to be sticking with its plan to raise rates consistently into sufficiently restrictive territory as inflation is proving stickier than expected in regions such as France and Germany. Despite this, energy prices continued to fall over the month, improving consumer sentiment. The Stoxx 600, an index of 600 publicly traded companies across Europe, gained 1.7% this month, reflecting positive consumer sentiment. This gain continues to reflect the narrative that the chances of a deep recession have become lower in the Eurozone compared to mid-2022.

With the re-opening of the Chinese economy now in full swing, a rapid consumption-driven expansion is expected. It comes as the country had accumulated a large amount of savings during Covid lockdowns which now can meet pent-up demand in the market. Despite this, Chinese equities retraced some of the gains reported in January throughout February, with rising geopolitical tensions playing a large part. The Chinese economy is likely to still have room to recover in the coming months.

Risks such as the size and longevity of interest rate hikes, the market shock from the fall out of the collapse of SVB, as well as continued geopolitical pressures remain prevalent. However, the continued strength of economic data, especially that coming out of developed regions, leaves room for optimism.

Change for Bonds in Portfolios

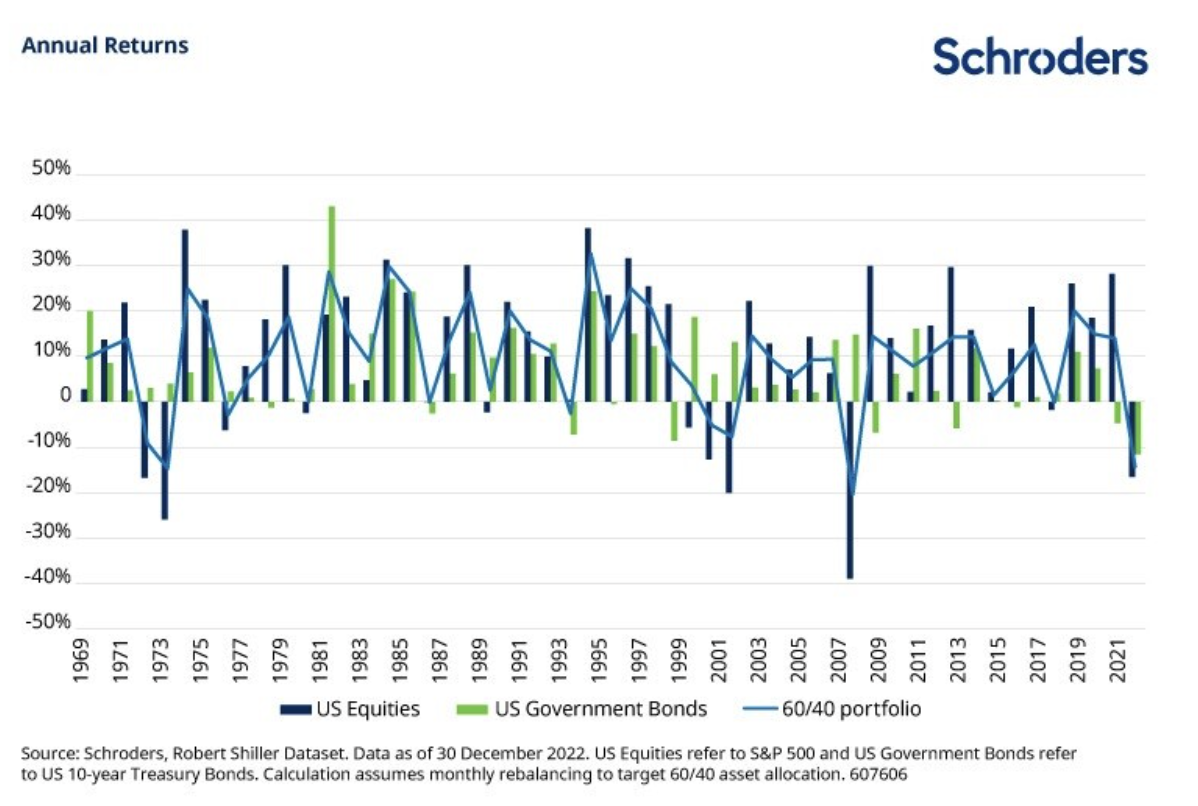

Bonds have traditionally been thought to offer diversification for investors in their portfolios alongside their equity allocation. Their diversification benefit stems from the thought that bonds have different characteristics from equities in the sense that where equities represent ownership in a company, bonds are loans of a company or government with predetermined interest rates, payment due date, maturity date and face value that the borrower will repay. As the return profile of bonds has far fewer uncertain variables than in comparison to equities, they have been generally considered less risky.

In the past, a portfolio of 60% equities and 40% bonds had been generally successful in achieving the outcome of providing investors with positive returns during most years. The bond characteristics have historically provided investors with protection in their portfolios as bonds and equities reacted differently to market conditions and therefore during times when equities drew down, bonds were able to provide a better performance and vice versa as depicted below.

However, during 2022 there had been a positive correlation between the performance of bonds and equities (the very last part of the graph above) as the economic conditions drove both asset class valuations lower, which has been a rarity (positive correlations when both asset classes appreciated in value has however happened quite often).

The 2022 year we were faced with a change in the economic environment, due to the increase in inflation, growth uncertainty and geopolitical tensions which have led to the development of some major trends. These trends include central banks have/will prioritise controlling inflation above growth and challenges to globalisation and supply chains.

These trends will continue to impact the performance (and correlation) of equities and bonds. It is still uncertain how sticky inflation will be, which is the dominant trend that negatively impacted both asset class performances. Should inflation be more persistent, it will likely lead to continued variation in bond performances. Not all classes of bonds react the same way to inflation, specifically longer-dated bonds generally have a higher duration, which indicates a bond's sensitivity to interest rate changes, and are therefore more susceptible to a decrease in their valuation due to the higher interest rates (inherently higher inflation) – but also may offer an opportunity for gains should we eventually enter a rate cutting cycle.

Short-duration bonds, however, have a much more limited sensitivity and during 2022 the average ultra-short-term bond fund was down only 0.1%, while the broader bond universe reported double-digit declines.

While the current strong labour markets of some of the major economies have been supportive of economies it has also raised uncertainty regarding the extent to which central banks may continue to raise interest rates to combat inflation during 2023. This indicates that a more proactive approach may benefit investors seeking the benefits of bonds in their portfolios this year. Investors may also benefit from other strategies to aim to achieve diversification in their portfolio with exposure to asset classes such as commodities which are driven by inflation, and un-constrained dynamic strategies that seek to harvest returns from systematic exposures, and which benefit from macro volatility.

Russia – Ukraine War: One Year on

The 24th of February 2023 marked the one-year anniversary of the Russian invasion of Ukraine. While the war is still ongoing, it has already had deep and lasting effects far beyond the battlefield, with economic, social, and political consequences. From an economic perspective, it is important to understand what effects have already been felt, where we currently stand, as well as what the future may look like.

In Ukraine, their economy contracted by 30% in 2022. In Russia, the economy shrunk by 2.15% during 2022. This was much better than expected at some stages during last year with the World Bank predicting a contraction of 11.2% in April of 2022. Despite the better-than-expected performance of the Russian economy, a contraction was still experienced when growth of 3% was predicted before the start of the year. Russia risks another ‘lost decade’ with a long period of stagnation highly probable before any sight of recovery is seen.

Beyond the two countries involved, the war has slowed post-pandemic recovery in developed and emerging markets as strong ripple effects have been felt globally. Russia and Ukraine are key to the global economy as their produce is important to supply chains running efficiently. Both countries are major exporters of key agricultural commodities wheat, barley, and corn. In addition to this, Russia is also a key exporter of fertilizer (Russia accounts for about 15% of global nitrogenous fertilizer exports) used across many farming and manufacturing activities worldwide. Ukraine's inability to effectively produce and export these commodities and sanctions against Russia have driven up food prices globally and has further fuelled the inflation fire, which Central Banks have been targeting to combat by raising interest rates.

Russia is also one of the world’s largest producers of oil. The outbreak of the war caused a large spike in oil and gas prices with sanctions being placed on Russia preventing any imports of Russian oil and gas by several major economies. The impact of these sanctions on oil and gas prices has however been eased in recent times which has been driven by efforts from European countries to secure alternative sources, backed up by conservation efforts as well as a mild winter. With oil and gas prices having somewhat stabilised (the spot price for brent crude reached a high of close to $124 at the end of May 2022 and has steadily decreased to around $81 currently), this will help ease supply chain pressures globally and should help Central Banks as they continue to try and rein in inflation.

There are numerous possibilities, not all likely, that might bring the conflict in Ukraine to an end. A ceasefire may be one of the more likely ways that this war could end with the 2015 Minsk agreement potentially providing the blueprint for this. French president, Emmanuel Macron, pointed to the use of this previous agreement between the two countries as the “only path on which peace can be built.” Other possible endings to this war may include a peace deal, a Russian victory, or a Russian retreat.

While the prices of key commodities have somewhat eased, going forward, challenges will certainly remain as geopolitical tensions remain escalated and no clear knowledge of what Russian President, Vladimir Putin’s, endgame is. While we are certainly not in the clear, it is likely markets have already priced in a lot of the damage caused by the war, as over a year has passed economic players have adjusted to the global challenges created by Russia’s attack on Ukraine.

Sources

JP Morgan: Monthly Market Review

Nasdaq February 2023 Review and Outlook

U.S. Equities Market Attributes February 2023

FTSE 100 falls on earnings drag; still logs best Feb in four years

European shares slip on sticky inflation fears, but still end Feb higher

SVB Financial: What Went Wrong, and What Happens Next?

Regime shift: what it means for strategic asset allocation

Why Stocks Generally Outperform Bonds

Here’s the stuff about bonds you were always too bored to learn about. Inflation means you have to

2022 was the worst-ever year for U.S. bonds. How to position your portfolio for 2023

After a Terrible Year for Bonds, the Outlook is Better

Bonds Booming in 2023 After Worst Year Ever

The ripple effects of Russia's war in Ukraine continue to change the world

XBR/USD - Brent Spot US Dollar

Russian economy shrank 2.1% in 2022, much less than expected

The Cost of War: Russian Economy Faces a Decade of Regress