The Pinnacle: December 2023

December 2 0 2 3 • I S S U E 36

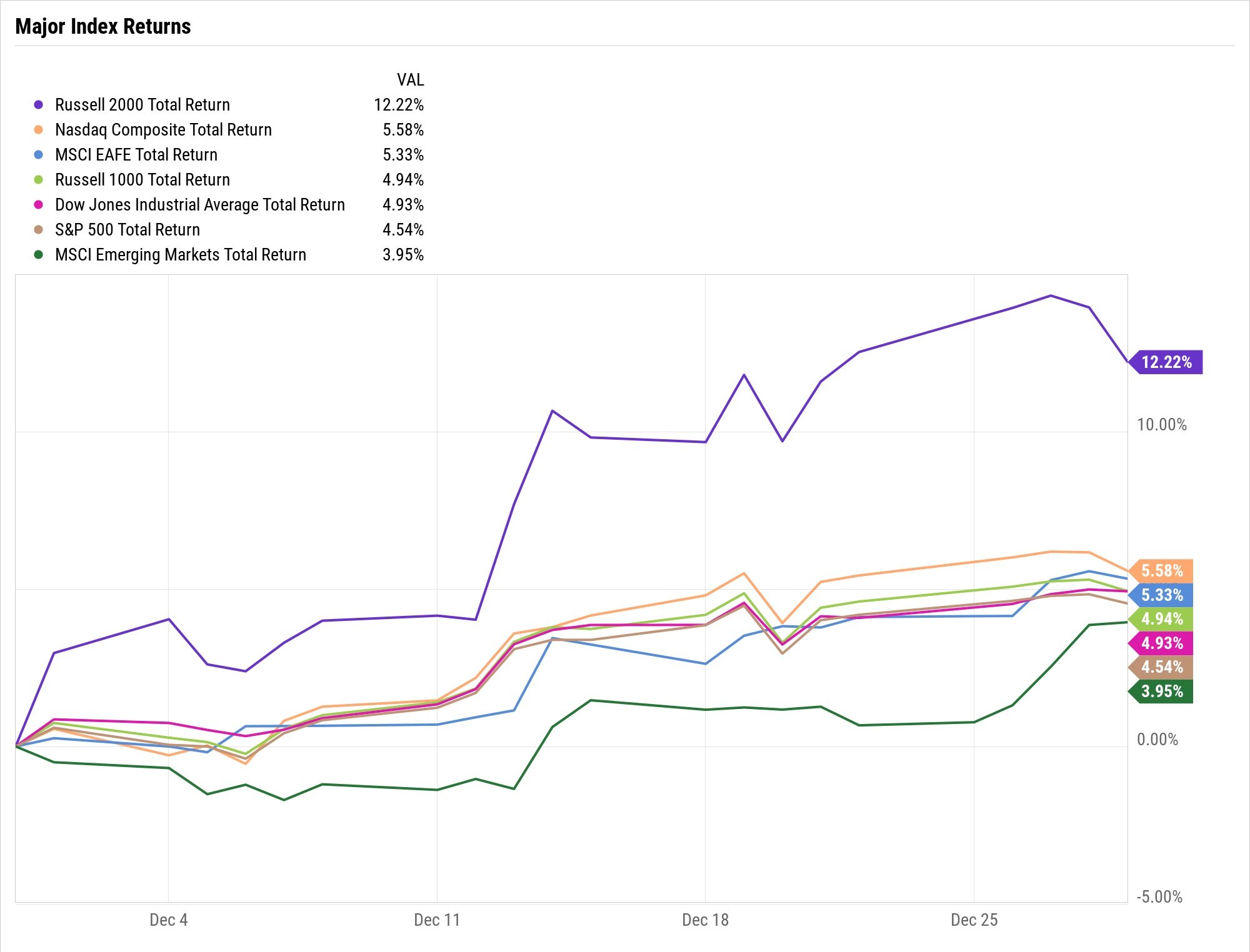

December Markets

The markets showed resilience in December despite continued macroeconomic headwinds, especially on the geopolitical front. Strong gains were recorded across major indices and inflation rates declined further increasing hopes of earlier rate cuts in 2024.

US

Amidst the highs of the festive period, the S&P 500 finished strong with a one-year return of 24.23% as the month’s gains ended at 4.24%. This is an opposite outcome to the decline it faced in December 2022.

Source: YCHARTS

Federal Reserve Chair Jerome Powell acknowledged recent progress on inflation and unemployment in his latest remarks, though warned against complacency. While reaffirming the Fed's commitment to bringing inflation down to its 2% target, Powell emphasised a cautious approach to monetary policy and effective communication with the public as regards stance on policy changes.

The December 2023 jobs report came as a surprise to some economists, including those with optimistic predictions. There was a spike in Government and healthcare jobs as The Bureau of Labor Statistics, BLS, reported the addition of 216,000 jobs, higher than the 173,000 addition from November.

Eurozone

The STOXX Europe 600 Index ended the year up 12.6%, posting its best performance since December 2021 and its seventh straight weekly gain in a row. The increased demand for bonds led to a fall in yields, especially longer-dated bonds. The German 10-year bond yielded 1.80%, the Italian 10-year BTP yielded 4.00%, and the French 10-year OAT yielded 1.95%. The fall in inflation rates led to lowered expectations for ECB rate hikes and increased optimism about rate cuts coming sooner than expected.

Investors are left on edge as the ECB seems a bit divided on its approach to rate hikes as inflation falls below 3%. While the unanimous target remains 2%, there are advocates for a dovish approach and advocates for a hawkish approach. Those with dovish sentiment expect rate cuts sooner rather than later while those with hawkish sentiment have a more negative outlook. The unfolding of this debate has left investor sentiment cautious despite growing optimism.

UK

The FTSE 100 and FTSE 250 ended the year up 3.8% and 17% respectively. Ten-year bonds dropped from 4.25% at the beginning of the month and ended at 3.75% by the end of December. Headline inflation (Consumer Price Index) fell to 3.9% down from 4.6% a month prior. Core inflation dropped to 5.1% from 5.7% previously. The fall in inflation fuelled optimism for a faster-than-expected fall to the bank's 2% inflation target. As predicted by analysts, the Bank of England (BoE) in its December 14th meeting kept rates unchanged at 5.25%

Commodities

Gold rose to 1.32% in December and ended the year at about $2,068.28 per ounce. Copper rose by 1.5% for the month. Brent Crude ended the year at $80.23 per barrel and WTI at $75.84 per barrel.

Conclusion

2023 could be summed as a better-than-expected year but that ended on an optimistic note. Though market conditions still remain impossible to fully predict and challenges do remain, events such as likely central bank rate cuts provide room for optimism.

2024 Market Outlook

The general feeling towards 2024 is a positive one. While there are and will be challenges there are reasons to be optimistic. 2023 ended off on a strong note which has certainly aided in increasing optimism for the year ahead. As mentioned, there are however challenges, with geopolitical tensions and economic slowdowns in some regions continuing to be on investors’ minds.

US Federal Reserve

In early 2022, the Fed embarked on a tightening cycle where they continued to raise the Federal funds rate through July of 2023. As the impact of the rising rates became more prominent in the middle of 2023, this led to a reduction in the pace of hikes as they acknowledged the impact of the rate hikes on the economy.

December came with signs of inflation cooling further and the Fed held rates steady. Some experts have interpreted this move as the end to what has been an aggressive hiking cycle.

The Federal Reserve held their last meeting for 2023 on the 13th of December and the outcome of the meeting can offer investors some cue about the new year. While the Fed maintains their unwavering commitment to bringing inflation down to the target 2%, the recent inflation trends hint that hikes are likely over.

Economists from Goldman Sachs are of the opinion that the 2024 global economy will perform better than general predictions. Jan Hatzius, Chief Economist at Goldman Sachs, says Fed cuts are unlikely before Q4 and predictions of a lowered rate in March are overly optimistic. He also says, the risk of a recession in view is on the low side and predicts a 15% possibility of this happening in 2024.

2024 US Elections

Data suggests the elections have very little impact on the market long-term. For instance, the S&P 500 historically experiences positive returns in election years, regardless of who wins.

Also, economic factors like unemployment and inflation trends have a stronger impact on the economy than elections. However, in the short term, periods leading to the elections bring increased volatility to the market. Policy proposals, campaigns, and polling data can lead to price fluctuations.

Strategists from J.P. Morgan are of the opinion that though elections obviously have major effects in other ways, they have little bearing on the path the market takes.

Denise Chisholm, director of quantitative market strategy at Fidelity Investments is of the opinion that investors should not be making big changes in their portfolio because of an election.

It's important to maintain a long term view of investments as this helps one to avoid making emotional decisions in response to the short-lived volatility that accompanies elections. This allows you to harness compounding power and gain returns that outlast short-term fluctuations.

Eurozone and UK Outlooks

The European Central Bank (ECB) and Bank of England (BoE) are approaching the year with optimism and clear vigilance. With inflation coming down but not quite there and macroeconomic headwinds remaining prevalent, the ECB's focus remains on bringing inflation down to 2%.

Experts predict the ECB is unlikely to raise rates in the first half of the year. Possible cuts are also expected if weaknesses in the economy persist and become a greater concern than inflation.

In the UK, inflation is higher than the Eurozone though also with signs of easing. Like the ECB, many predict the BoE may leave rates consistent with potential for cuts within the year.

Conclusion

As a default, financial markets are volatile and subject to fluctuations. Despite worries around inflation, geopolitical tensions, and economic slowdowns, 2023 was a resilient year. This can be considered a reason why it's often better to set long-term goals to gain the most out of one's investment as well as to maintain a disciplined approach to investing.

Sources

Monthly Market Wrap: December 2023

Euro area inflation rises less than expected in December

Sluggish UK economy gathers a bit of pace at the end of 2023

London stocks finish higher ahead of Christmas break

Monthly Market Wrap: December 2023

US elections toss twist at markets fixated on Fed, economy

Investors' Election Year Worries Could Be Overblown, Experts Say