The Pinnacle: April 2024

April 2 0 2 4 • I S S U E 40

April Markets

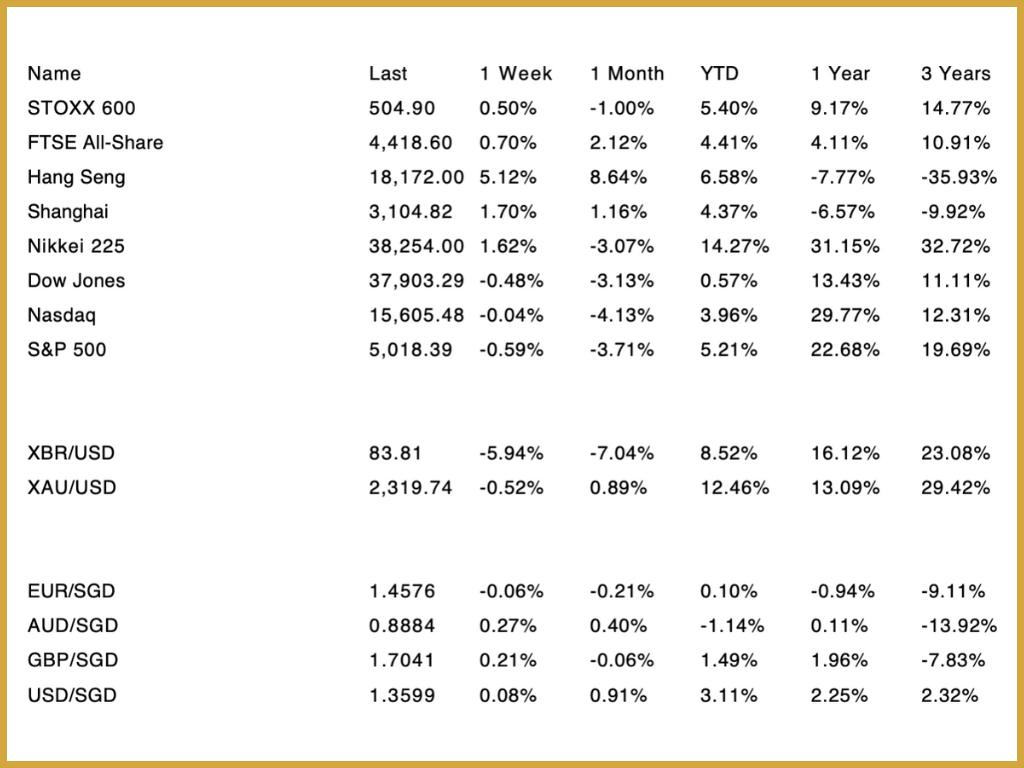

Source: investing.com (2 May 2024)

After a strong start to the year markets experienced a downward correction in April. Global Developed market equities were down 3.7% for the month. Emerging market equities produced solid performance gaining 0.5% for the month. Fixed income experienced a downward move with global bonds falling 2.5% for the month.

In the US, the Dow Jones, NASDAQ, and S&P 500 have lost 3.13%, 4.13%, and 3.71% respectively over the last month. A slightly hotter-than-expected inflation number meant that the higher-for-longer narrative in terms of interest rates played into investors thoughts during the month. Headline Inflation came in just ten basis points higher-than-expected at 3.5% year-over-year (YoY) for March, up from 3.2% previously. Bonds struggled as the market pushed back its expectations of the timing of the first rate cut by the US Federal Reserve (Fed) to further back in the year, while still expecting that two rate cuts will arrive this year. Two-year Treasury yields rose by 40-basis points to 5.0% and ten-year Treasury yields rose by 47 basis points to 4.7%. While yields rising does represent bond prices falling as an inverse relationship exists between the two it also opens up the opportunity for investors to lock in higher yields over different time periods.

Equities experienced a pullback during April in the Eurozone, with the STOXX 600 index down 1.00% over the last month. Despite this, the European Central Bank (ECB) continues to be ahead of the game compared to their developed market counterparts in terms of the fight against inflation and nearing their 2% target. Headline inflation came in as expected at 2.4% YoY for March, down from 2.6% previously. Core inflation, which excludes the volatile food and energy prices, also fell as expected to 2.9% YoY for March, down from 3.1% previously. These positive inflation numbers raised hopes that the ECB might cut rates at their next meeting in June. The market is believed to be currently pricing in a 70% chance of this cut occuring, with even higher probabilities for July and September cuts priced in.

Unlike its developed market counterparts, the UK produced positive equity market performance over the month of April. The FTSE All-Share gained 2.12% over the last month. The equity market benefitted from its high exposure to energy and commodities, contributing significantly to the positive returns over the month. Headline inflation dropped to 3.2% YoY for March, down from 3.4% previously. Along with the ECB, there is greater confidence of an earlier rate cut by the Bank of England (BoE) compared to the Fed. Slowing inflation and some, although slow, growth has caused the market to price in the first rate cut for September.

In China, equities recorded gains for the month of April with the Shanghai Composite up 1.03% for the month. These gains came as investors focused on signs of an improving economic picture in the region. Analysts also believe gains have been driven by investors rushing to avoid missing out on rallies caused by more supportive policies from the Chinese government. Notably, strong performance come from Hong Kong during the month with the Hang Seng Index up 4.85%. These gains reflect a change in sentiment in the region after dismal performance in 2023.

Market performance in April emphasised the need for investors to ensure they have a degree of protection against inflation in their portfolios. While there are risks associated with inflation coming in higher than expected, any market moves as a result should be viewed as short-term fluctuations. Despite a tough month it is important to maintain a long term view, while not allowing short-term moves in the market to disrupt a long-term strategy.

Commodities Update

Commodity prices traditionally tend to be greatly affected by the global macroeconomic environment. Therefore, in turn, commodity prices are also able to give one insight into the current state of the global economy. With factors such as wars in Ukraine and the Middle East currently affecting the global economy it is important to take a closer look at commodity prices to gain insight into how the market is reacting to these headwinds.

With both the Russia-Ukraine War and Israel-Hamas War ongoing it is important to ask what effect wars would traditionally have on commodity prices. While wars themselves are thought to mostly not have a direct impact, they do however create the conditions conducive to price rises in commodities. This often relates to supply chain disruptions which can cause commodity shortages in certain parts of the world, with the likes of oil and agricultural commodities especially affected. Precious metals, such as gold, have traditionally been viewed by investors as a “safe haven asset” during times of turmoil. Therefore, an event such as a war that can have serious macroeconomic impacts, is capable of causing a “flight to safety,” potentially meaning the price of an asset like gold will rise.

In terms of the current environment, economic theory has somewhat played out but not completely. Oil supply has not been disrupted to a great extent by the Israel-Hamas War. UBS Strategist, Giovanni Staunovo, stated that “Geopolitical risk premiums tend not to last if supply is not actually disrupted.” At the time of writing (2 April 2024), Brent Crude is currently trading around $83.80 per barrel and is up 8.46% year-to-date (YTD). While no great jump is expected, some pressure on supply does remain, with some analysts forecasting the oil price to remain above $80 per barrel for the rest of 2024.

Source: Reuters

At the time of writing the price of gold has risen 12.24% YTD. With the precious metal reaching a new all-time high this year it is thought that inflation remaining stickier than expected in the US has put upward pressure on the price. Traditionally, gold has an inverse relationship with real interest rates. With interest rates in the US currently thought to be on hold investors will closely watch how gold responds once the US Federal Reserve (Fed) begins to cut rates. Additionally, as it is widely regarded as one of the main reasons for the price rises so far this year, investors will continue to watch whether inflation in the US remains sticky Within the 3% to 4% range or if it starts edge closer to the Fed’s 2% target.

In terms of other commodities, silver is up 11.35% YTD while copper futures are up as much as 17.28%. In terms of agricultural commodities, US wheat futures are down 3.28% YTD while US cotton futures are down 4.88% YTD. Notably, US Cocoa Futures are up just under 91.00% YTD. The large increase in the price of Cocoa is driven by a shortage of the commodity in West Africa. The region, which accounts for 80% of the world's Cocoa supply, has been affected by a climate-change-induced drought, damaging their crops and in turn reducing output.

Going forward, commodities, as always will be an important asset class to watch to gauge how investors are reacting to different macroeconomic challenges. While the movements in cocoa prices are an outlier, it does illustrate the fact that certain commodities can respond dramatically to different economic challenges. It is important to remember that while economic theory is useful, what traditionally happens is not always how the market acts in real time.

Sources

Review of Markets over April 2024

Euro zone inflation steady at 2.4%, keeping June rate cut in play as economy returns to growth

China stocks rally as investor 'fear of missing out' spreads

Hong Kong stocks are back from the dead. Here’s why

Oil futures fall as fears of a wider Middle East war fade

Oil price forecasts raised as supply risks persist

Gold price forecast for spring 2024: Here's what experts predict

Gold hits new high as investors seek hedge against stubborn inflation